Investment Diversification: What It Is and How To Do It

Many or all of the products featured here are from our partners who compensate us. This influences which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money.

The investing information provided on this page is for educational purposes only. NerdWallet does not offer advisory or brokerage services, nor does it recommend or advise investors to buy or sell particular stocks, securities or other investments.

Diversification definition and examples

Diversification is a common investment strategy that entails buying different types of investments to reduce the risk of market volatility. It's part of what’s called asset allocation, meaning how much of a portfolio is invested in various asset classes.

Three of the most common asset classes are stocks, bonds and cash (or cash equivalents). To achieve diversification, investors will blend dissimilar assets together (like stocks and bonds) so that their portfolio does not have too much exposure to one individual asset class or market sector.

Investors have many investment options, each with its own advantages and disadvantages. Some of the most common ways to diversify your portfolio include diversification by asset class, within asset classes and beyond asset class.

» Want easy and automated diversification? Learn about investing through robo-advisors.

Diversification example

Say you invested all of your money only in Apple stock (AAPL). Apple is a technology company, so this would mean that your asset allocation would be 100% equity (or stock) all in the technology sector of the market. This is a risky approach because if Apple stock prices were to slump due to unforeseen circumstances, your whole investment portfolio would suffer the consequences. You might diversify within the technology sector by investing in other tech stocks, but if the whole technology sector is negatively impacted, your portfolio would still take a big hit.

To appropriately diversify a portfolio, you’ll need to include stocks from many different sectors. Even still, you may also want to include bonds or other fixed income securities to protect against a dip in the stock market as a whole.

Diversification is the simplest way to boost your investment returns while reducing risk. By choosing not to put all of your eggs in one basket, you protect your portfolio from market volatility. Diversification may look a little different for each investor. Factors such as time horizon and risk tolerance should be assessed on a case-by-case basis to determine how to best construct each portfolio to fit the individual needs of each investor. Luckily, there are plenty of tools available that help make it easy to diversify your investment accounts.

Diversification by asset class

The three main general asset classes in an investment portfolio are stocks, bonds and cash.

Stocks (or equities) allow investors to own a piece of a company. Stocks offer the highest long-term gains but are volatile, especially in a cooling economy.

Bonds (or fixed income) pay interest to investors who lend money to a company or government. Bonds are income generators with modest returns but are usually weaker during an expanding economy. Generally, bonds have an inverse relationship with stocks.

Cash (or cash equivalents) is the money in your savings account, pocket or hidden under your pillow. In terms of risk and return, cash is low on both counts. Cash can buffer volatility or unexpected expenses and acts as “dry gunpowder” to invest during opportune times.

There are other asset classes such as real estate (property), commodities (natural resources, precious metals) and alternative investments. These asset classes usually have lower correlation to the stock market and as such can be effective to aid in diversification.

» Want to see a list of potential investments? Here are the best investments for any age or income.

Diversification within asset classes

After asset level diversification, investors can further the process by categorizing the main general asset classes into sub-classes or breaking them down into more detail.

Diversification beyond asset class

Diversification can extend beyond traditional asset classes found in typical investment accounts. Investment accounts have non-guaranteed returns since they are subject to market fluctuation. However, there are other product types such as pensions, annuities and insurance products that can provide guaranteed income streams and returns. For reduced risk, investors often diversify their portfolio by spreading their investment dollars among these different product types as well.

» What's a small-cap ETF?

The benefits of diversification

Diversification provides what professionals call a “free lunch” — reducing overall risk while increasing the potential for overall return. That’s because some assets will perform well while others do poorly. But next year their positions could be reversed, with the former laggards becoming the new winners. Regardless of which stocks are the winners, a well-diversified stock portfolio tends to earn the market’s average long-term historic return. However, over short-term periods that return can vary widely.

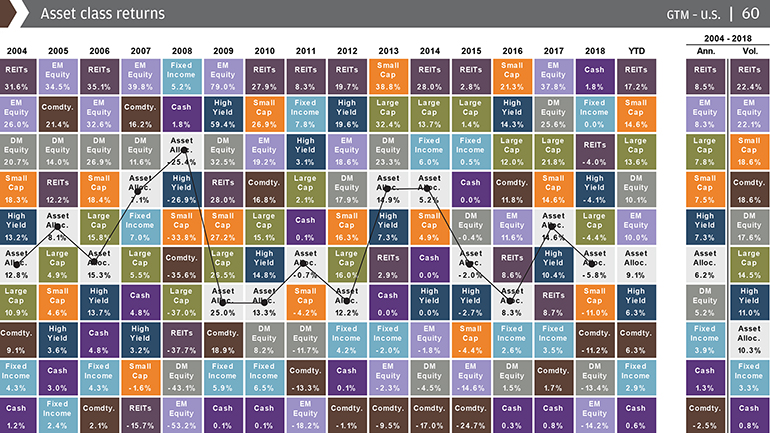

Below, the graphic from J.P. Morgan shows the variability of different types of investments from 2004 to 2018. Navigating the market’s fickle nature, the “asset allocation portfolio” (a diversified portfolio with a mix of investments) stays in the middle of the pack, achieving an annualized return of 6.2% over the time period and evening out the ride.

Owning a variety of assets minimizes the chances of any one asset hurting your portfolio. The trade-off is that you never fully capture the startling gains of a shooting star. The net effect of diversification is slow and steady performance and smoother returns, never moving up or down too quickly. That reduced volatility puts many investors at ease.

Reducing risk through diversification

While diversification is an easy way to reduce risk in your portfolio, it can’t eliminate it. Investments have two broad types of risk:

Market risk (systematic risk): These risks come with owning any asset — yes, even cash. The market may become less valuable for all assets, due to investors’ preferences, a change in interest rates or some other factor such as war or weather.

Asset-specific risks (unsystematic risk): These risks come from the investments or companies themselves. Such risks include the success of a company’s products, the management’s performance and the stock’s price.

You can radically reduce asset-specific risk by diversifying your investments. However, do what you might, there’s just no way to get rid of market risk via diversification. It’s a fact of life.

You won’t get the benefits of diversification by stuffing your portfolio full of companies in one industry or market––this can create higher risk. How terrible would it have been to own an all-bank portfolio during the global financial crisis? Yet some investors did — and endured stomach-churning, insomnia-inducing results. The companies within an industry have similar risks, so a portfolio needs a broad swath of industries. Remember, to reduce company-specific risk, portfolios have to vary by company industry, size and geography.

How to build a diversified investment portfolio

Creating a diversification strategy for your portfolio diversification may sound difficult, especially if you don’t have the time, skill or desire to research individual stocks or investigate whether a company’s bonds are worth owning. Most securities can be purchased individually or in a collection, such as through a mutual fund, index fund or exchange-traded fund (ETF). For example, simple, low-cost, "set it and forget it" ETFs or mutual funds — especially index funds and target-date funds — can get a portfolio diversified quickly and safely while reducing risk. Robo-advisors are another option that can help with portfolio diversification.

Here's a diversified portfolio example that shows how diversification might look in your own portfolio.

A commonly used option for passive investors is an ETF or mutual fund based on the S&P 500 index, a broadly diversified stock index of 500 large, industry-leading American companies. It’s diversified by industry and even though the companies are based in the U.S., a significant portion of their sales is generated overseas. Investing in the S&P 500 is an example of how you can gain benefits of immediate diversification with just one fund.

» Learn more: How to invest in the S&P 500

The downside: Such funds are concentrated in stocks. To gain wider diversification, you may want to add bonds to your portfolio. Plenty of diversified bond ETFs exist, and they could help balance out the volatility of a stock-heavy portfolio.

Virtually all large investment companies offer some index and bond funds, and they’re readily available for individual retirement accounts and 401(k) plans.

» MORE: How to invest your IRA

Other options include target-date funds, which manage asset allocation and diversification for you. You set your retirement year, and the fund manager does the rest, typically shifting assets from more volatile stocks to less volatile bonds as you approach retirement. These funds tend to be more expensive than basic ETFs because of the manager’s fees, but they can offer value for investors who really want to avoid managing a portfolio at all.

With these options, you can achieve the benefits of diversification relatively simply and affordably.