NerdWallet, Inc. is an independent publisher and comparison service, not an investment advisor. Its articles, interactive tools and other content are provided to you for free, as self-help tools and for informational purposes only. They are not intended to provide investment advice. NerdWallet does not and cannot guarantee the accuracy or applicability of any information in regard to your individual circumstances. Examples are hypothetical, and we encourage you to seek personalized advice from qualified professionals regarding specific investment issues. Our estimates are based on past market performance, and past performance is not a guarantee of future performance.

We believe everyone should be able to make financial decisions with confidence. And while our site doesn’t feature every company or financial product available on the market, we’re proud that the guidance we offer, the information we provide and the tools we create are objective, independent, straightforward — and free.

So how do we make money? Our partners compensate us. This may influence which products we review and write about (and where those products appear on the site), but it in no way affects our recommendations or advice, which are grounded in thousands of hours of research. Our partners cannot pay us to guarantee favorable reviews of their products or services. Here is a list of our partners.

Financial Goals: Where to Begin

Saving for retirement starts with prioritizing your financial goals. Check these three goals off your list first.

Dayana is a former NerdWallet authority on investing and retirement. She has written for The Associated Press, The Motley Fool, Woman’s Day, Real Simple, Newsweek, USA Today and more. She has written and contributed to several personal finance books and has been interviewed on the "Today" Show, "Good Morning America," NPR, CNN and other outlets.

Arielle O’Shea leads the investing and taxes team at NerdWallet. She has covered personal finance and investing for 15 years, previously as a researcher and reporter for leading personal finance journalist and author Jean Chatzky. Arielle has appeared as a financial expert on the "Today" show, NBC News and ABC's "World News Tonight," and has been quoted in national publications including The New York Times, MarketWatch and Bloomberg News. Email: <a href="mailto:[email protected]">[email protected]</a>.

Many or all of the products featured here are from our partners who compensate us. This influences which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money.

The investing information provided on this page is for educational purposes only. NerdWallet does not offer advisory or brokerage services, nor does it recommend or advise investors to buy or sell particular stocks, securities or other investments.

You’ve got plans. Stuff you want to do, things you want to buy, milestones you hope to meet.

At one end of the spectrum are immediate financial commitments, such as paying for groceries and next month’s rent or mortgage. At the other are long-term financial goals like retirement, which is years, or even decades, away. In between are wants and needs such as homes, cars, vacations, dining out, medical expenses and education costs.

When you have a finite amount of money — as most people do — achieving your financial goals takes planning. Here's how to set and prioritize your goals.

The three most important financial goals

Let’s start with three goals that should be top priorities on everyone’s list.

Goal 1. Set aside $500 to cover emergencies

The gold standard of emergency funds is to save up enough money to cover three to six months’ worth of living expenses, so that a layoff or an injury won’t land you in a deep debt hole. (Note, we’re talking about necessary-to-survive expenses like food and shelter.)

But for many people, scraping together several months’ worth of expenses in savings is too onerous right out of the gate. So shoot for $500 as a starting point, which would at least help with an unexpected car repair or other big bill. We don’t want you to indefinitely postpone making progress on the next two goals because you’re stuck behind the first savings hurdle.

Where should you keep your emergency fund? Someplace safe (FDIC insured), liquid (as in easily accessible via withdrawal or funds transfer in case of, you know, an emergency), and where it might even earn a little interest. A high-yield savings account at an online bank meets all of these criteria.

If you have an employer-sponsored retirement plan — such as a 401(k) or 403(b) (the version for nonprofit and public service employees) — and your company matches any portion of your contributions, sign up right now. (See your human resources department for the paperwork.) Contribute at least enough money to get all the matching funds your company offers.

The most common employer match is 50% of contributions, up to 6% of salary. That could translate into free money worth 3% of your salary each year.

Discussing credit card debt may seem out of place in a guide about investing and retirement planning. It’s not. It’s simple math.

If you carry a balance on your credit card and pay an interest rate at or above the high single digits, you’ll save more in interest by paying that off than you stand to earn through investing. (The exception: the aforementioned employer match, because that is a guaranteed return on your money.)

Once you’ve got those first financial “to dos” out of the way, it’s time to get down to the business of planning.

Deciding how much of each paycheck to direct toward which savings goal — the near-term and the long-term ones — is a balancing act. But it’s absolutely doable.

We’re firm believers in the “pay yourself first” school of thought, by directing a portion of your paycheck into your Future Self’s piggy bank right off the bat. Saving 10% of your pretax income is a good place to start; 15% is golden. If you’re contributing to your 401(k), you’re on your way, since both your contribution and your employer’s contribution count toward that 10% or 15% goal.

Then, as the retirement savings machinery thrums on autopilot in the background, you can focus on your more immediate wants and needs. For those nonretirement goals, ask:

1. How much will it cost? Achievable savings goals start with accurate cost estimates. Research the price of things on your shopping list to ensure your goal is in the ballpark of reality.

2. How soon do I need the money? Divide that cost by the number of months, weeks or years between now and your deadline. If that number makes you do a double take, consider adjusting the goal (substituting a less costly alternative) or the time frame (pushing the big vacation out until next year).

3. Where should I put my savings? The answer here depends on the kind of time frame you landed on in answer to the last question.

If you plan to reach your goal in less than five years, you should consider short-term investments like online savings accounts, CDs or money market accounts.

You might wonder why stocks aren’t on that list. Although the stock market has rewarded long-term investors with generous returns, over short periods of time it is prone to wild swings.

For example, say you’d invested $100 in 2008, right before the Great Recession began. Your balance would’ve dropped to just $43 at the bottom. Now imagine how you’d feel if that $100-turned-$43 had been earmarked for the next summer’s vacation or your kid’s freshman-year tuition, due that fall.

The lesson: Money you need within the next five years should not be invested in the stock market.

On the other hand, money you don’t need to touch for the next five years or more is a candidate for stock investment. That’s because you have more time to wait out the market’s dips and ride the eventual recovery.

Practical matters

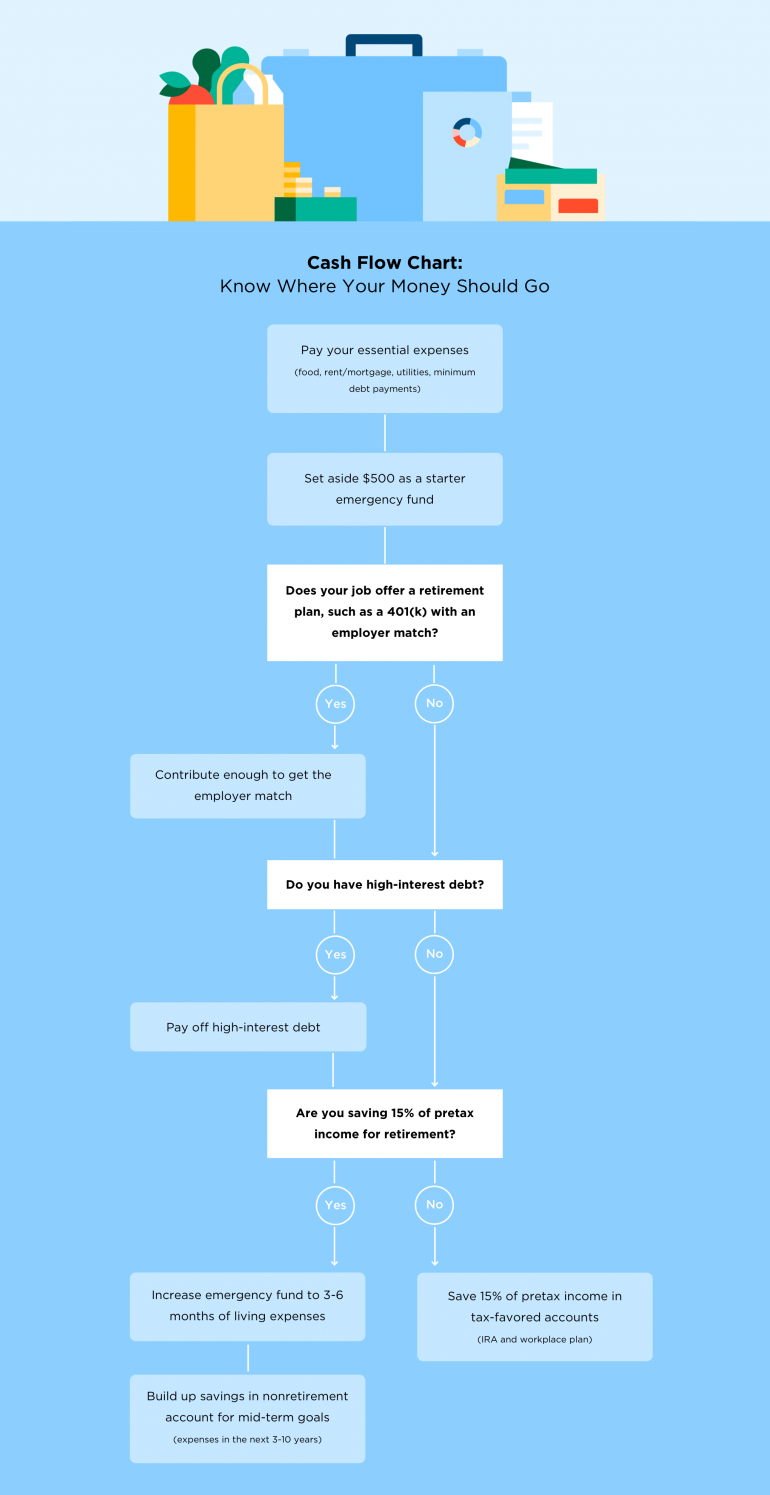

What to do when there’s only so much paycheck to go around? We made this handy flowchart to show you how to direct your dollars when you’ve got multiple financial goals and competing priorities.

Take a screenshot. Print it out and post it on the fridge. Doodle daily affirmations in the margins (“College, here she comes!” “Debt, your days are numbered…”) and use it as a reference whenever there’s a question about what to do with your spare change.