What Is a UCC Filing?

Many or all of the products featured here are from our partners who compensate us. This influences which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money.

A Uniform Commercial Code filing, also known as a UCC filing, is a document that lenders use to establish their legal right to assets that a borrower uses to secure a loan. This notice allows the lender to seize the borrower’s collateral in the case of default.

UCC filings can cover a specific piece of collateral, or lenders can file a blanket lien, which applies to all of a borrower’s assets. Filing a UCC lien is a common practice among lenders when they issue small-business loans.

The Uniform Commercial Code is a set of laws that govern commercial transactions across the U.S. These uniformly adopted state laws help promote and simplify interstate business. Article 9 of the Uniform Commercial Code provides guidelines for transactions secured by assets or property, resulting in the term UCC filing.

How does a UCC filing work?

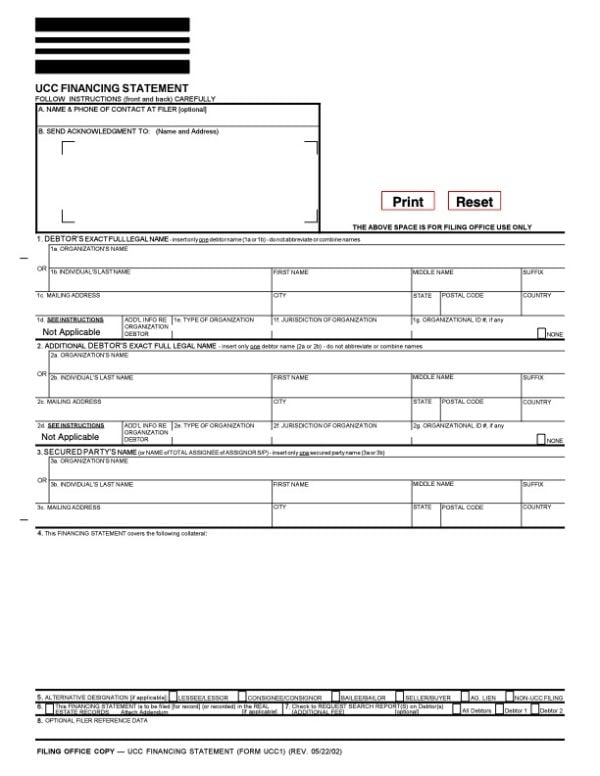

A UCC filing gives a lender the first-position right to claim a borrower’s collateral in the case of loan default. UCC liens are typically filed using a UCC financing statement, also called the UCC-1 financing statement.

This document is submitted to the secretary of state’s office in the state where the business (i.e., the borrower) is located. The UCC-1 financing statement identifies the assets or properties the lender has claim to, and lets other creditors know of its security interest in that collateral.

UCC-1 financing statement for New York state.

UCC liens can be filed on a range of personal and/or business assets, including but not limited to real estate, inventory, receivables, vehicles, machinery and equipment.

Once a UCC lien is filed with the secretary of state’s office, it becomes public record, meaning anyone can go online and search for active filings.

Although the specifics can vary from state to state, UCC filings usually last for five years. If your loan is still active after that period of time, your lender can apply for a continuation of the lien. The lender can also file amendments or addendums to the statement, if necessary.

Types of UCC filings

There are two types of UCC filings that can be used to secure a business loan.

UCC lien on specific collateral. Lenders can file a UCC lien on specific pieces of collateral, such as real estate or equipment. If you default on your business loan, the lender can claim these assets to recoup its losses. However, it can’t claim any other company assets.

Blanket lien. This type of lien covers all of a business’s assets, not just a specific piece of collateral. If you default on your loan, the lender can claim (and/or sell) any of the assets it needs to cover its losses.

The UCC filing a lender uses can vary based on a variety of factors, including the type of business loan, your company’s qualifications and the individual lender itself.

Specific collateral liens tend to be used for special-purpose loans, such as equipment or inventory financing. Blanket liens, on the other hand, are commonly used for standard bank loans, SBA loans and online loans.

How a UCC filing impacts your business

In general, a UCC filing is not bad for your business — it simply serves as an official notice to other creditors that your lender has a security interest in one or all of your assets. However, UCC filings can impact your business credit, risk your company’s assets and/or hinder your ability to get future financing.

Impact on business credit. Although your credit report will show any UCC filings taken out on your business within the last five years, these liens don’t typically impact your business credit score. If you make late payments or default on your loan, though, your credit can be negatively affected.

Risk your company’s assets. When a lender files a UCC lien, some or all of your assets (depending on the type of lien) are at risk if you fail to pay back your loan. As long as you repay your lender, your assets will remain safe. On the other hand, if you don’t repay your loan, the lender can seize your assets to recover its losses.

Hinder your ability to get future financing. A UCC filing indicates that a lender has the first position to claim your collateral in the case of default. If you decide to apply for additional financing, your new lender can search to see if your business has any liens against it. In many cases, lenders are hesitant to take second position on a company’s assets and may deny your business loan application — or offer limited funding — if you have an active UCC filing.

How to remove a UCC filing

Even if you repay a business loan, any UCC filing on that financing will remain active until it expires — usually after five years. Removing a UCC lien on a loan that you’ve repaid can help you qualify for other business funding options.

You can remove a UCC filing by asking your lender to submit a UCC-3 form to terminate the lien.

If you find a UCC lien listed on your credit report that shouldn’t be there, you can contact the credit bureau (e.g., Experian, Dun & Bradstreet) and file a dispute to have it removed.